04/07/2021

0

Views

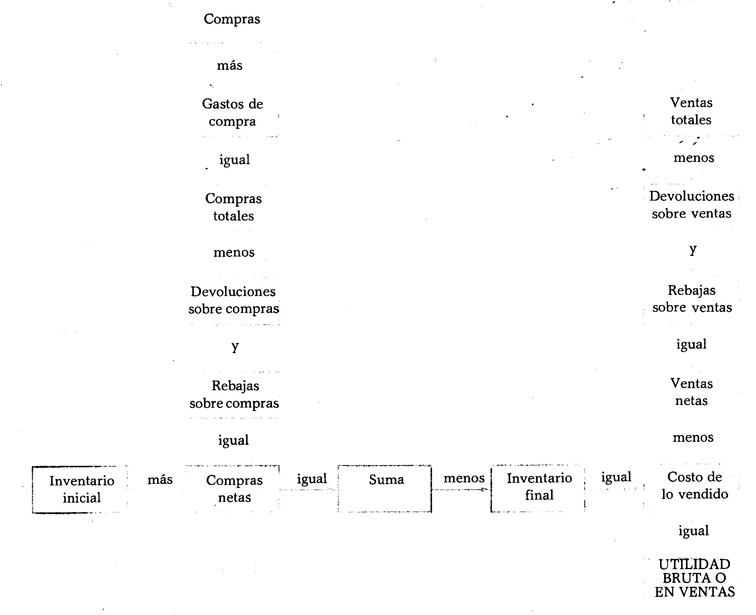

Profit on sales. Once the value of net sales and the cost of sales have been determined, profit on sales is determined by subtracting the value of cost of sales from net sales.

Example:

Considering the net sales and the cost of what was sold in the previous cases, the profit on sales would be:

The profit from sales is also called gross profit.

Observation. When the cost of goods sold is greater than the value of net sales, the result will be the loss on sales or gross loss.

Use of columns. As in the Balance Sheet, the Profit and Loss Statement uses four columns to record the amounts. The following indicates in which column the value of each of the elements that makes up said status is noted.

First column. In this column you must enter the values of purchases, purchase expenses, returns on purchases and discounts on purchases.

Second column. In this column, the values of returns on sales, discounts on sales and total purchases must be entered.

Third column. In this column you must enter the values of total sales, beginning inventory, net purchases and ending inventory.

How to obtain the profit in sales