0

Views

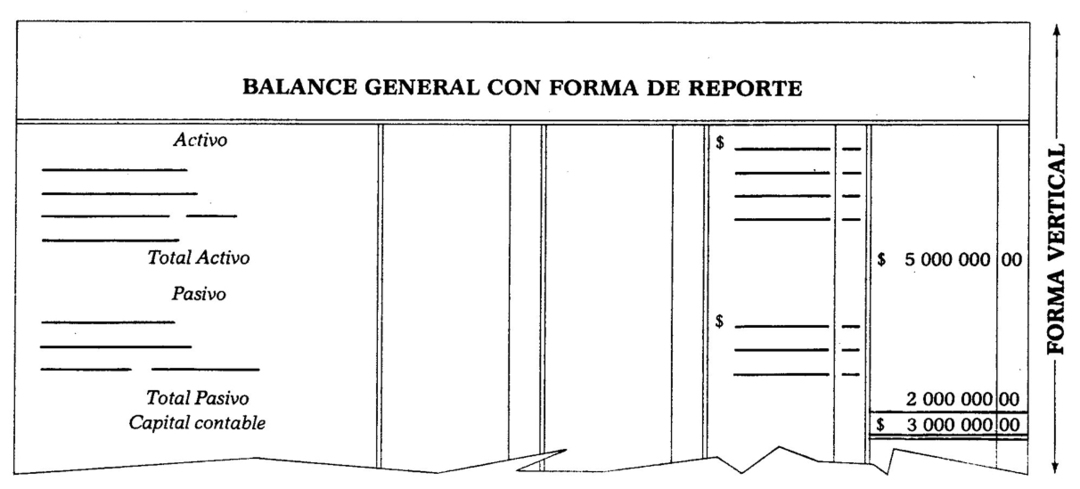

It consists of classifying Assets and Liabilities, on a single page, in such a way that at 76 The sum of the Assets can be vertically subtracted from the sum of the Liabilities, to determine the stockholders' equity. Example:

According to the above, we see that the Balance Sheet with report form is based on the formula:

Assets - Liabilities = Capital that expressed by means of literals remains:

A - P = C

78 This previous formula is known as the capital formula.,;

In order to illustrate the. Previous explanations a model of the Balance Sheet is presented on the next page in report form.

79 The Balance Sheet must be transferred to the Inventory and Balance Sheet book.

The Inventory and Balances book has a special line, distributed as follows: a large space intended for indicate the names of the accounts, and four equal columns with subdivision for pesos and cents, in which the quantities.

For the Balance to have a good presentation, the following indications must be taken into account:

80 1. The name of the business should be noted in the center of the sheet, on the first line.